All That Glitters Is Gold

“An object in motion tends to remain in motion along a straight line unless acted upon by an outside force.” Sir Isaac Newton

Last September, we noted that gold had many structural reasons to soar. Well, soar it has, eclipsing the previous highs from way back in September 2011. Gold is up more than 28% since we published our LPL Research blog, Time for Gold to Shine? in early September 2019, easily outpacing the 7% gain from the S&P 500 Index over the same time period.

Think about this: 2020 is the first year since 1979 to have both gold and the S&P 500 make new highs during the calendar year. What happened the last time? Gold added another 17% and the S&P 500 was up 26% in 1980. It is widely believed that stronger gold likely means something is wrong in the markets and investors are more defensive, but it might not be that simple.

The US dollar and gold were linked until 1971 when President Richard Nixon ended dollar convertibility to gold, but since then, both gold and stocks have been higher 23 out of 49 years. Incredibly, in 12 of those 23 years, both assets were up at least 10%, with 2019 being the last time it happened. All of this suggests that the two assets can trend higher together, and it isn’t always a bearish development to see gold strong. In fact, we remain bullish on both stocks and gold here, as the two can trend higher together.

Although there isn’t one lone reason gold is back to new highs, there are at least 10 reasons why gold very well could remain strong.

- The US dollar is at its lowest level in more than two years. Historically, gold and the US dollar trade inversely. We continue to expect a lower trending US dollar as we discussed in our July 23 LPL Research blog, Dollar Weakness May Continue.

- Growing concerns over US-China relations.

- COVID-19 uncertainty and potential economic weakness.

- European data is quickly improving, and Europe is doing a great job containing COVID-19, thus potentially strengthening the euro—which may pressure the US dollar lower.

- Record monetary stimulus. The Federal Reserve (Fed) balance sheet exploded to $7 trillion recently, from $4 trillion before COVID-19.

- Nearly $15 billion worth of negative sovereigndebt globally.

- Record trade and budget deficits.

- 0% interest rate policy is likely here to stay.

- Negative real-rates, making gold’s 0% interest look pretty good.

- Huge government spending programs may spur inflation.

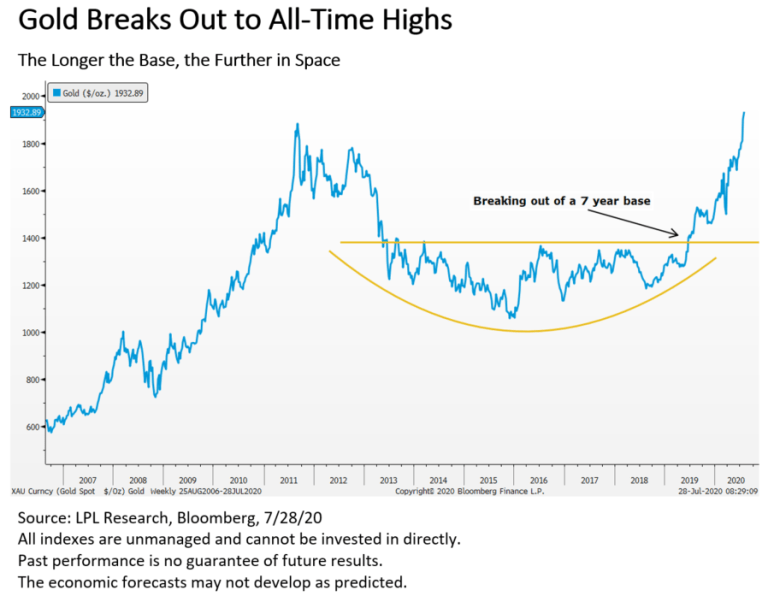

“More than 300 years ago, Sir Isaac Newton taught us that an object in motion will likely stay in motion,” explained LPL Financial Chief Market Strategist Ryan Detrick. “There are many fundamental reasons to expect gold to do well, but maybe the easiest argument is that fighting an asset as it’s making new highs after nearly a decade without any new highs has been a losing fight throughout history.”

As shown in the LPL Chart of the Day, gold based for seven years and broke out late last year, ushering in the new highs we are seeing now. There’s an old technical saying that “the longer the base, the further in space,” and this played out quite well this time, as gold based for years before the surge higher. Technically, gold still looks like it will continue to do well, while fundamentally there are still many tailwinds. We remain bullish on gold in this environment.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All index and market data are from FactSet and MarketWatch.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use – Tracking 1-05038225