Funding Your Future with a Fixed Annuity

A fixed annuity is a contract between you and an annuity issuer, usually an insurance company. In its simplest form, you pay money to the annuity issuer; the issuer invests the funds and pays the principal and its earnings back to you or to your named beneficiary. What’s fixed about a fixed annuity? The issuer guarantees (subject to its claims-paying ability) a minimum rate of interest on your investment and a fixed benefit amount if you elect to annuitize.

When is an annuity appropriate?

Annuity contributions are made with after-tax dollars and are not tax deductible. That’s why it’s often advisable to fund other retirement plans first.

However, if you’ve already contributed the maximum allowable amount to other plans and want to save more toward your retirement, an annuity can be an excellent choice. There’s no limit to how much you can invest in an annuity, and the funds grow tax deferred until you begin taking distributions.

Once you begin withdrawing from your annuity, you’ll pay taxes (at your regular income tax rate) only on the earnings, since your contributions to principal were made with after-tax dollars. Like a qualified retirement plan, a 10% tax penalty may be imposed if you withdraw from an annuity before age 59½.

Annuities are designed to be very-long-term investment vehicles. In most cases, if you take a withdrawal, including a lump-sum distribution of your annuity funds within the first few years after purchasing your annuity, you may be subject to surrender charges imposed by the issuer. However, many companies allow options for withdrawals or distributions without incurring a charge. As long as you’re sure you won’t need the money until at least age 59½ and you understand the costs (including fees) involved, an annuity is worth considering.

Two distinct phases to an annuity

There are two distinct phases to an annuity contract: the accumulation phase and the distribution phase.

In the accumulation phase, you’re putting money into the annuity. You can choose to pay your premiums in one lump sum, or you can make a series of payments over time. These payments can be of equal amounts made at equal intervals, or of variable amounts at irregular intervals, depending on the terms of the contract.

Annuities may be either immediate or deferred; the terms simply refer to when the distribution phase begins. Immediate annuities are typically purchased with a single payment and the distribution phase usually begins within a year of the purchase. While deferred annuities may be purchased with a single lump sum premium payment, they are most often purchased with a series of periodic payments. The distribution period is deferred until some time in the future.

In the distribution phase, you begin taking money out of the annuity. You may withdraw some or all of the money in lump sums, or you may annuitize. Subject to the claims-paying ability of the issuer, annuitization provides a guaranteed income stream for either a specified period or for life.

Why buy an annuity?

- To provide income to supplement what you receive from Social Security, pension plans, and other employer-sponsored retirement

- To create a lifetime income

- To maintain financial independence. For example, you can use annuity funds to pay for long-term care expenses and stay in your own home, rather than rely on your children for

- To invest for any specific purpose or long-term goal, such as providing a legacy for your heirs or making a charitable gift.

- To grow funds on a tax-deferred

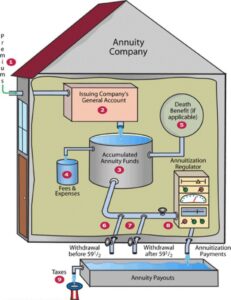

How a Fixed Deferred Annuity Works

- In the accumulation phase, you (the annuity owner) send your premium payment(s) (all at once or over time) to the annuity issuer. These payments are made with after-tax funds, and you may invest an unlimited amount.

- The annuity issuer places your funds in its general * Your annuity contract specifies how your principal will be returned as well as what rate(s) of interest you’ll earn during the accumulation phase. Your contract will also state what minimum interest rate applies.**

- The compounding interest on your annuity accumulates tax You won’t be taxed on these earnings until funds are withdrawn or distributed.

- The issuer may collect fees to manage your annuity account. You may also have to pay the issuer a surrender fee if you withdraw money in the early years of your annuity.

- Your annuity contract may contain a death benefit or other provisions for a payout upon the death of the annuitant. (The annuitant provides the measuring life used to determine the amount of the payments if the annuity is annuitized. As the annuity owner, you’re most often also the annuitant, although you don’t have to be.)

- If you make a withdrawal from your deferred annuity before you reach age 59½, you’ll not only have to pay tax (at your ordinary income tax rate) on the earnings portion of the withdrawal, but you may also have to pay a 10 percent premature distribution tax, unless an exception applies.

- After age 59½, you may make withdrawals from your annuity without incurring any premature distribution Since annuities have no minimum distribution requirements, you don’t have to make any withdrawals. You can let the account grow tax deferred for an indefinite period. However, your annuity contract may specifiy an age at which you must begin taking income payments.

- To obtain a guaranteed** fixed income stream for life or for a certain number of years, you could annuitize which means exchanging the annuity’s cash value for a series of periodic income payments. The amount of these payments will depend on a number of factors including the cash value of your account at the time of annuitization, the age(s) and gender(s) of the annuitant(s), and the payout option chosen. Usually, you can’t change the payments once you’ve begun receiving them.

- You’ll have to pay taxes (at your ordinary income tax rate) on the earnings portion of any withdrawals or annuitization payments you

* These funds are invested as part of the general assets of the issuer and are therefore subject to the claims of its creditors.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

The information provided is not intended to be a substitute for specific individualized tax planning or legal advice. We suggest that you consult with a qualified tax or legal professional.

LPL Financial Representatives offer access to Trust Services through The Private Trust Company N.A., an affiliate of LPL Financial.

This article was prepared by Broadridge.

LPL Tracking #416948