How Corporate Bond Spreads Respond to Equity Market Volatility

An old Wall Street adage says bond markets are smarter than equity markets, so when stocks encounter volatility, investors often look to the bond market for clues about the potential severity of equity market weakness.

The option-adjusted spread (OAS), a key data point, adjusts a bond’s yield for any unique features of the bond in an effort to make various bonds more comparable to each other. Since US Treasury bonds are generally considered safe-haven assets, the OAS of corporate bonds as a group is often based on a comparison to Treasury yields to determine bond investors’ perception of credit risk. The OAS reflects the additional yield investors may require to compensate for the specific risks in corporate bonds.

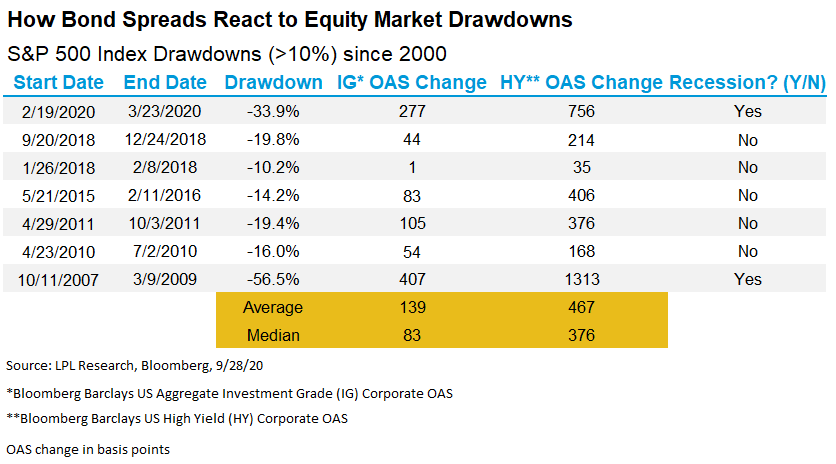

However, not all drawdowns in equity markets are the same, and bond investors oftentimes sniff this out, which can keep bond spreads from widening as much as they often do during periods of economic turmoil. As shown in the LPL Chart of the Day, equity drawdowns that are followed by a recession have encountered the largest increases in spreads:

Unfortunately due to the limited availability of daily OAS index data, we weren’t able to include the dot-com bubble in our study. However, we were able to capture two serious credit crises in history: the early stages of the COVID-19 pandemic and the 2008 financial crisis.

Since the S&P 500 peaked on September 9th, IG and HY credit spreads have widened by 14 and 66 basis points, respectively, although we have not yet encountered a 10% drawdown as of September 25th. “We haven’t seen a major reaction from credit markets to the September volatility thus far,” noted LPL Chief Market Strategist Ryan Detrick. “While there may be more volatility in our future with the upcoming election, we’ll continue to monitor corporate spreads for any major warning signs for corporate credit and protracted weakness in stock prices.”

Spread widening can also have dramatic effects on a company’s ability to issue new debt to manage its cash needs. Since a company is able to issue debt only at the prevailing yield of its outstanding bonds in the market, wide credit spreads can cause a serious cash crunch for corporations, and even create liquidity-driven bankruptcies—an added motivation for the Federal Reserve to provide relief to boost the economy through monetary policy.

While we believe Federal Reserve Chair Jerome Powell and the Federal Open Market Committee (FOMC) have so far been able to effectively manage the liquidity crisis that affected credit markets in the early stages of the pandemic, members of the FOMC continue to emphasize the need for additional fiscal stimulus to manage the risks to the economy. Despite the inability of Congress to come to an agreement on a new stimulus bill thus far, we’re encouraged by the recent calls to resume negotiations in Washington. In our view, additional fiscal stimulus could support sustainable recoveries in US economic growth and corporate profits.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All index and market data from FactSet and Bloomberg.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use – Tracking 1-05060884