Small Business Optimism Falls to Recovery Low

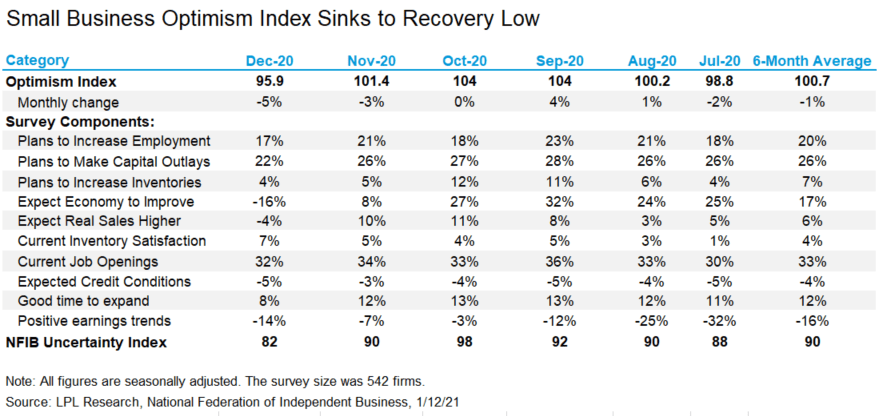

Rising COVID-19 cases and concern about the policy environment put a dent in small business optimism in the month of December, the index’s second straight monthly decline. As shown in the LPL Chart of the Day, the National Federation of Independent Business (NFIB) Small Business Optimism Index, a survey of more than 500 firms, declined in December to 95.9, falling below the long-term average index value since 1973 of 98. Further, 9 of the 10 index components declined, while only one—satisfaction with current inventory—managed to improve.

The rise in COVID-19 cases in the fourth quarter of 2020 and the subsequent rise in restrictions implemented by state and local governments have taken a toll particularly on small businesses, pushing the Uncertainty Index component of the survey 8 points below the 6-month average. Meanwhile, the rise in COVID-19 cases has coincided with the election of a new administration in Washington, DC, and the potential regulatory and tax changes that may come with it, adding further uncertainty.

“Small businesses are rightfully concerned about their business outlook as new COVID-19 cases continue to surge,” noted LPL Chief Market Strategist Ryan Detrick. “The widespread vaccine distribution should be the key to lifting us out of the pandemic; however, local restrictions used as a bridge during the rollout of the vaccine will create a tough environment for small businesses.”

While survey data has suggested a tough economic environment, the stock market has been signaling this uncertainty may be short-lived, at least for publicly traded small cap stocks. As of January 12, 2021, the Russell 2000 Index of small cap stocks has handily outperformed its large cap counterpart, the S&P 500 Index, by nearly 11%. In Weekly Market Commentary: Market Policy Projections for 2021, we explain that the increased prospects for additional fiscal stimulus may encourage rotation toward areas of the market that may respond positively to economic reopening, which includes small cap stocks.

Even though small cap stocks—and perhaps the broader market—could be due for a breather after such a strong post-election rally, we think the future for small caps is brighter than the survey results may be suggesting.

In this week’s Market Signals podcast and video, LPL Research talks about 2021 policy updates and the possibilities of higher taxes and more regulation, more stimulus, higher Treasury yields, and better stock performance in 2021.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All index and market data from FactSet and Bloomberg.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use – Tracking 1-05099136