Taking Stock at the Halfway Mark

It’s certainly been a wild ride for stocks in 2020. Barely past the halfway point, the year has already brought the worst pandemic to hit the US in over 100 years, an unprecedented government-induced recession as much of the country was locked down, some stomach-churning market volatility, and massive, unprecedented stimulus from policymakers totaling several trillion dollars—that’s trillion with a “t”.

The dizzying volatility began in late February with the fastest-ever bear market decline (going back to the inception of the Dow Industrials in 1896). It took just 19 trading days for the Dow to close more than 20% below its record high (February 19 through March 12). The S&P 500 Index fell 20% during the first quarter, one of the worst starts to a year ever.

After the March 23 low in the S&P 500, the record breaking continued as the S&P 500 staged its best 50-day rally since the inception of the S&P 500 more than 60 years ago. The strong snapback led to a 20% second quarter gain, the best for the index since the fourth quarter of 1998, and brought the S&P 500 to within 3% of a positive year as of June 30 based on total return.

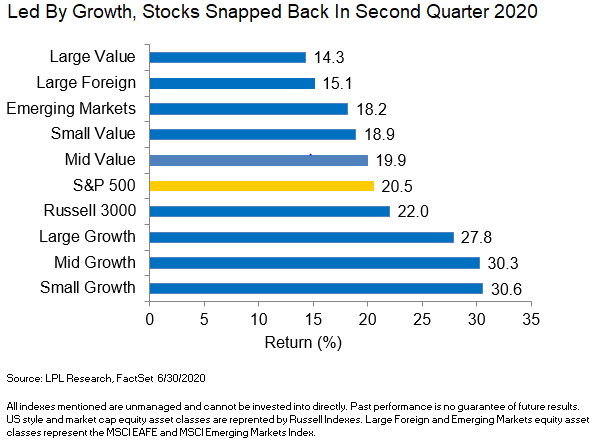

Growth stocks led the way, as shown in the LPL Chart of the Day, continuing their decade-long run of nearly uninterrupted dominance over value stocks as the Russell 1000 Growth Index trounced its Value counterpart during the quarter.

“The dominance of growth stocks is one of the biggest stories for the market in 2020,” noted LPL Financial Equity Strategist Jeffrey Buchbinder. “Stronger balance sheets, better earnings, and favorable positioning for the work-from-home trend suggest this historic run for growth stocks over the past decade may still have legs.”

The US continued its multi-year trend of outperforming non-US equity markets based on the MSCI EAFE and Emerging Market Indexes. And consistent with historical patterns coming off major market lows, smaller cap stocks outperformed their larger cap counterparts during the quarter.

Sector leadership looked similar to that of the last bull market from March 2009 through February 2020, with consumer discretionary and technology on top. These growth sectors are well positioned for the current environment, in our view, given the work-from-home trend and large allocation to internet retail within the consumer discretionary sector.

For more of our thoughts on the year, please listen to our latest LPL Market Signals podcast here.

Look for our Midyear Outlook 2020—an outlook for the economy, stocks, bonds, and the election—on July 14.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use | Tracking # 1-05030711