5 Lessons Learned About Rising Rates

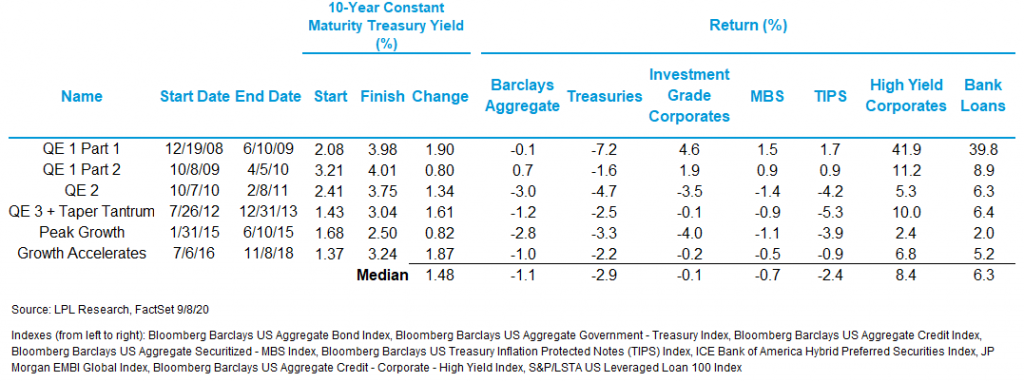

While the direction of the 10-year Treasury yield over the last cycle was decidedly lower, as shown in LPL’s Chart of the Day, there were still six extended periods where it rose at least 0.75%, and in two of those it rose almost 2%. Looking ahead, economic growth below potential, slack in the labor market, and an extremely supportive Federal Reserve (Fed) may limit rate pressure in the near term, but with interest rates already low and massive stimulus in place, we believe the overall direction is likely to be higher.

“Even in a falling rate period there are lessons from the last cycle about rising rates,” said LPL Financial Chief Investment Officer Burt White. “Among them: Careful when the Fed stops buying and sometimes the best defense is a good offense.”

While every economic cycle is unique, the last cycle highlighted these key takeaways about periods of rising rates:

- Careful when the Fed stops buying. The two drivers of rising rates last cycle were economic growth and Fed bond purchases, also known as quantitative easing (QE). The Fed buys bonds to keep rates down, but the start of Fed buying has actually been the time when rates rise—likely on expectations that the purchases would help strengthen the economy. These periods also often followed large rate declines either because markets anticipated the start of Fed buying or the economy was faltering. The takeaway: unless the economy is really taking off, any rising-rate period may pause for an extended period, or even reverse, when the Fed backs off bond purchases.

- Sometime the best defense is a good offense. Lower-quality, more economically sensitive bond sectors actually performed well during periods of rising rates during the last cycle. Rate gains were largely driven by economic improvement rather than a large pick-up in inflation, and that’s typically a good environment for sectors like high-yield bonds and bank loans. The downside is that these are much riskier bond sectors and don’t provide the potential diversification benefits of higher-quality bonds during periods of stock declines.

- Don’t expect TIPS to provide much resilience because of their inflation adjustment. Treasury Inflation-Protected Securities (TIPS) are high-quality bonds that have provided a little extra insulation against rising rates compared to similarly dated Treasuries when inflation expectations increased. TIPS prices are adjusted for inflation, but even with the adjustment, they are still very sensitive to rates.

- Investment-grade corporates can both hurt and help. If credit spreads narrow when rates are rising, investment-grade corporates can post some solid gains in a rising-rate environment, but if spreads are holding steady or even widening, they can be very sensitive to changes in Treasury yields, potentially (although not often) even more sensitive than Treasuries.

- Mortgage-backed securities (MBS) have not provided as much insulation as corporates, but they also have had less downside. While MBS have certainly outperformed Treasuries during periods of rising rates, they have not performed as well as investment-grade corporates. But they also have come with less downside, losing only 1.4% in their worst performing period compared to a 4% loss during the worst period for corporates.

With the Fed still providing strong stimulus and economic growth potentially poised to accelerate, we currently see an increased risk of rates moving higher. We are playing some offense with our equity exposure, which allows us to emphasize a focus on higher-quality bonds. Among bond sectors, we are emphasizing MBS and still prefer investment-grade corporates over Treasuries. History may not repeat, but if it rhymes, this positioning may help add resilience to a fixed income portfolio if rates extend their move off recent lows.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All index and market data from FactSet and MarketWatch.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use – Tracking 1-05053422