Emerging Markets Emerge this Week

U.S. Markets Lower

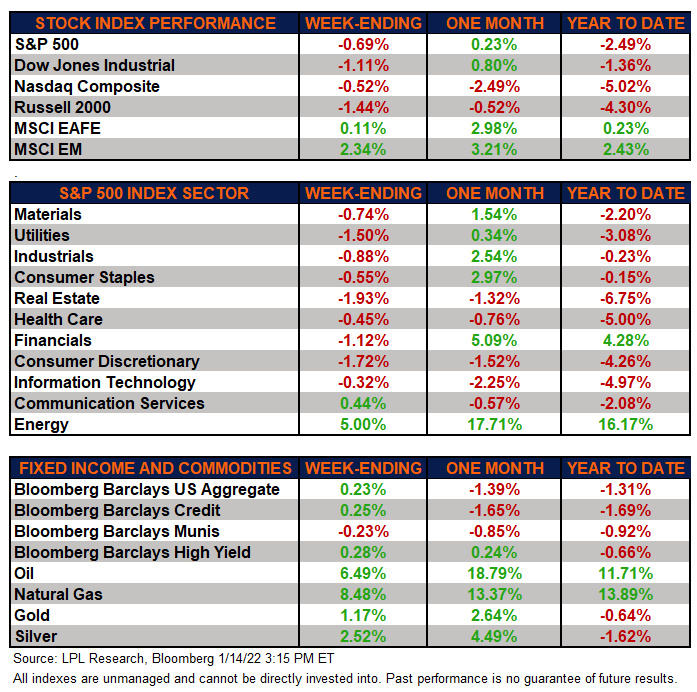

The major equity markets finished the week lower as concerns about inflation and higher interest rates continue to weigh on investors’ minds. A weaker than expected December retail sales report along with mixed big bank Q4 earnings did not help the market’s case for going higher. Energy led all sectors for the second straight week on the back of gradual OPEC supply production boosts that will, most likely, not keep up with worldwide demand.

International markets finished in the green this week. Emerging Markets, which were last year’s laggard on the back of concerns over Chinese regulation and real estate indebtedness, are leading the pack in 2022. Inexpensive valuations along with stimulus and potentially improved growth prospects have traders re-considering their position in the New Year.

Fixed Income Reverses Course

The Bloomberg Aggregate Bond Index finished higher and reversed some of last week’s declines. High-quality bonds had a rough December as traders sold off longer-term government bonds on inflation concerns and priced in a more aggressive timetable for Fed rate hikes. This sentiment carried over to high-yield corporate bonds, as tracked by the Bloomberg High Yield index, as these bonds gained ground this week reversing course from last week’s declines.

Solid Week for Commodities

Natural gas continues 2022 on a high note after gaining over 40% last year. This week, the commodity appreciated over 8%. In addition, oil had a solid start to the New Year, gaining over 6% for the week. The major metals also finished higher this week, following a difficult 2021 despite inflation concerns.

Economic Weekly Roundup

Retail Sales Disappoint

The U.S. Census Bureau reported that December retail sales declined more than economists expected. Increased prices in addition to surging Omicron cases exacted damage across the board as consumer activity waned. Holiday sales were pulled forward into November, exacerbating the declines. Wholesale prices rose, climbing almost 10% in the 12-month period for the biggest calendar-year rise in more than 10 years of collected data.

Highest Headline CPI in 40 years

The U.S. Bureau of Labor Statistics reported that the Consumer Price Index (CPI) rose 7.0% year over year in December. This was in line with expectations, however it was above the prior month and the eighth consecutive month above 5%. Core CPI (excluding food and energy) rose 5.5% year over year, slightly higher than forecasts, above November’s reading, and the highest level since 1990.

Small Business Optimism Improves

The National Federation of Independent Business’s (NFIB) Small Business Optimism Index inched higher in December and beat consensus expectations. The report showed that business owners believe that economic expectations will improve although the overall picture still shows slowing growth. As was the case for most of 2021, inflation and challenges hiring qualified workers continue to plague small businesses.

Jobless Claims Increase Again

Initial claims for unemployment insurance continue to come in near multi-decade lows. For the week ending January 8, they came in at 230K, which was higher than economists’ expected. The weekly total is the highest since November 12, and is likely related to the latest Omicron driven surge in COVID-19 cases. Continuing claims fell below 1.56M, the lowest level in almost 50 years.

The following economic data is slated to be released during the week ahead:

- Tuesday: National Association of Home Builders January Housing Market Index

- Wednesday: December building permits and housing starts

- Thursday: Weekly initial and continuing unemployment claims, December existing home sales

- Friday: December leading indicators

Next week, 38 S&P 500 companies will report their fourth quarter 2021 earnings results

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. All market and index data comes from FactSet and MarketWatch.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

For a list of descriptions of the indexes referenced in this publication, please visit our website at lplresearch.com/definitions.

This Research material was prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use – Tracking #1-05233060